How to Build Savings: A Forced Savings Plan You Can Stick To

19 Jan 2024 •

5 min read

By Ben BudgeDirector, Senior Adviser & Head of Advice

TABLE OF CONTENTS

Are you living with the daily stress of debt hanging over your head? Maybe you have a big investment to make or you want to buy a house in the next few years.

A forced savings plan may be the answer you’re looking for.

The average savings of Australians is just 5% of their income, leaving many vulnerable to financial shocks. But what if there was a way to save automatically, without having to think about it? Forced saving can help you gain control of your finances. Using this easy technique, you can start taking positive steps towardsgetting out of debt or being able to afford that big purchase you have been eyeing.

Key takeaways

Forced savings plans have financial and psychological benefits, particularly in that they free up your time and willpower.

Choose one main goal to focus on, although micro savings goals are ideal for creating good financial habits and preventing credit card debt

Set up your savings using locked accounts or use a separate bank to your spending accounts – this can prevent you spending it on anything except your goal

What is a Forced Savings Plan?

A forced savings plan is also known as ‘automatic saving’ or a ‘commitment to invest,’ and does just that. It is a series of automatic transfers that are in place to ensure your savings goals in yourfinancial plan are being met, and your investment strategy is active.

You want to build your emergency fund, reach your home deposit faster, or retire confidently? A consistent savings plan is a big key to success, at any stage of life.

Essentially, you are paying your goals first, before other expenses have a chance to claim your income. This kind of savings plan prioritises consistency and reduces dependence on willpower. Your automatic transfers act as a silent but effective financial coach, diligently accomplishing your saving goals over time.

The Benefits of Forced Savings Plans

Savings plans in general are incredibly beneficial. This is because setting goals and taking action makes you far more successful than just hoping you’ll get the hang of it. You might notice both financial and psychological benefits to a personal savings plan.

Financially, you’ll enjoy more freedom when it comes to your budget.By automating the process, you won’t need to rely on sheer willpower or memory to make progress. And the money is put aside before you’re tempted to spend it for other purposes.

This approach frees up mental energy and time, allowing you to focus on other financial decisions. As you see consistent growth, you will enjoy a tangible sense of progress, which motivates you to continue.

“Do not save what is left after spending, but spend what is left after saving.” – Warren Buffet

Psychologically, having a forced savings account has been shown to lead to increased savings over time and reduce casual spending. You’ll enjoy more confidence and peace of mind, and hopefully more willpower to spend on other priorities! This discipline can help break generational cycles of financial mismanagement and give you the opportunity to enjoy new financial possibilities.

How to Create Your Savings Plan

Here’s a step-by-step checklist for setting up a solid savings plan:

1. Define Your Big Goals & Milestone Goals

Big Goal: Clearly identify your main financial goal. For example, saving for a 20% house deposit on an $800,000 property. Make sure that it’s just one attainable savings goal! As soon as you achieve your goal, set your next goal to keep the momentum going.

Milestone Goals: It can be helpful to have milestones for your primary goal along the way that you can celebrate. Calculate when you want to reach particular milestones. Making it a game and competing with yourself makes it more fun!

Micro Goals: If you have smaller goals in mind, such as a laptop or even Christmas presents, set up additional micro goal transfers. This can prevent you from creating credit card debt.

2. Set up automatic transfers

Check your monthly budget: Make a realistic budgetto calculate how much of each salary you can afford to save. In order to achieve your savings, you might have to be a lot stricter on discretionary spending habits, such as subscriptions and take-away meals.

Choose an amount to transfer from your checking account to a high-interest savings account each payday before bills.

Know your time frame: Once you know how much you can save each paycheck, calculate how long it will take to reach your goal. Take our house deposit target – a 20% deposit is $160,000. If we can afford to save $500 a week, we can set our deadline to achieve that objective in just over 6 years, saving up to $26,000 each year (without potential interest earnings).

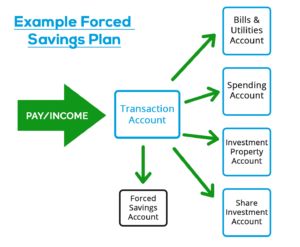

Put your plan into action: For most banks or credit unions, you can easily set up automatic transfers using online banking or their mobile app. Consider setting up transfers that are difficult to edit, a locked bank account that you can’t easily access, or using a different financial institution to your spending account.

Round up Transactions: Some online savings apps and bank accounts will round up your everyday purchases to the nearest dollar and transfer the difference to your savings account. These automatic roundups can really add up over time.

3. Other Ways to Use Automatic Savings Plans

The concept of a forced savings plan is simply automating your goals to happen without your direct input and willpower day after day. You can apply this same principle to other financial situations, most commonly debts and investing. You’ll already experience ‘forced saving’ through superannuation, and some people also use it by paying more tax and then getting their tax return back (we don’t recommend this as you have much less control over the results, and it usually gets spent rapidly).

Debts: Rather than putting as much of your non-essential budget into your automated savings, you can pay down debt much more rapidly by automatically directly more of your cash flow towards outstanding debts. A little bit more makes a huge difference over time.

Investing: If you don’t need to save cash, you can set up a money transfer to an investing or brokerage account, or use an app like Raiz to automatically build an investment portfolio. This is an excellent option for starting to build your wealth with what you have now.

How to Increase Your Savings By Reducing Spending

Automatic savings, combined with cost saving techniques, can be a game-changer to increase the amounts of money you can put away. These techniques are particularly useful to feel in control of your debts and bills.

Eliminate High-Interest Debt First

To make your savings goals even more effective, combine them with a proactive approach to clearing your debt. Credit card debt, in particular, has high interest fees that can rapidly eat away at your money before you realise it. Check that your payments are not only covering the charges and interest, without making a big dent in your balance.

If you have these high-interest debts, your priority should be to pay these debts off first. Take some of that savings plan money and put it towards extra payments off your credit cards or other debts – this is saving you money in interest, so it is very worth it!

Consolidate high-interest debt

If you have many individual loans, you might be able to reduce monthly payments and free up money for savings by consolidating loans to a lower interest rate. Seek advice from a financial expert to see whether you can roll yourdebts into one loan. This will consolidate the repayments and reduce interest and charges.

Overpay monthly bills

Pay slightly extra than your regular payment on your bills like utilities and mobile. Overpaying by a few dollars each month will accumulate a surplus before you know it. Eventually, you’ll have a month where the bill does not need to be paid at all, freeing up extra money for other purposes or savings.

You can also use this on your home loan. It can be powerful snowball effect to pay off your mortgage more quickly, save on interest, and accumulate equity faster.

Windfalls or Loose Change Can Be Important Too

Treat unexpected income, like bonuses or tax refunds, as an opportunity to boost your savings. Avoid putting them into the pool of your regular funds if you can help it. It’s a little old-fashioned, but a basic ‘piggy bank’ approach can bring real rewards. Put your loose change into a jar or tin on a regular basis. Make a note on the tin about what that money is for – mine is ‘Europe Holiday’ – so you can get excited about what that money will be used for. Once you have filled the piggy bank, taking it to the bank and adding it to your savings will be extremely satisfying.

Superannuation and Forced Savings in Australia

“Put it into a tax-deferred account. Over time, it will begin to amount to something. This is such a no-brainer.” – Charlie Munger

The concept of forced savings in superannuation is a powerful tool for retirement funding – that’s why the government continues to strengthen it over time. The superannuation guarantee is currently 11% of your wage, however the superannuation cap allows additional contributions up to the value of $27,500.

Salary Sacrificing into Superannuation

Salary sacrificing into superannuation builds on this. Additional concessional (pre-tax) contributions are a way that you can work with the superannuation system to increase your retirement savings.

This method is particularly advantageous as it encourages long-term saving for retirement and saves you from paying tax on any concessional contributions, up to the cap amount.

It is easy to set up. Simply discuss how much superannuation you want to be withheld before tax by talking to your employer.

Note: Additional concessional contributions shouldn’t be confused with other methods of salary sacrificing such as employee benefits involving cars or other expenses.

By Ben BudgeDirector, Senior Adviser & Head of Advice

Ben is a founding partner of My Wealth Solutions and is passionate about helping his clients achieve their financial goals.