Sarah jumped out of her car outside a renovated worker’s cottage in the inner-north suburbs of Brisbane. Her first investment property. The real estate agent met her on the footpath, holding a big SOLD sticker. Together they took a video for Instagram of Sarah pasting the sticker across the ‘For Sale’ sign on the front fence.

Getting into investing in property had been a challenging journey for Sarah, requiring a fair bit of determination and number-crunching. But she was very happy knowing that this house matched her capital growth strategy. After all her research on negative gearing, tenancy rates, and property trends in the suburb, this was a symbol of her hard work and financial acumen.

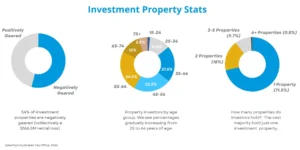

Sarah’s story is an example of many Australians who take the journey in property investing. Around 2.2M Australians own investment properties (that’s around 8.4% of the Australian population), but fewer Australians are getting into property investing year on year. So how can you get started in a way that will ensure your financial success?

Grab your keys and let’s unlock the door to your own investment property journey.

Property is considered to be a stable and relatively lower-risk investment (when compared to the stock market for example), which makes it a popular investment choice. As a financial advisor, I often recommend a diversified portfolio that includes a combination of property and shares, but you should compare the two to see which suits your situation best.

Real estate values in Australia have shown a steady increase, with Vanguard’s 2023 Index Chart showing annual growth of 7.3% each year since 1993. However, this does not always mean that property will be a profitable asset that will increase your wealth. Property values can be impacted by a large number of factors (such as location, mining, immigration, and the media). The success of your investment depends primarily on the property location, as well as on the quality of the asset.

Ultimately, an investment property has one purpose: to make you a profit, either now or in the long term. Consider your purchase from a logical and mathematical perspective. Unlike when purchasing your dream home, you shouldn’t get your emotions involved. What matters is which one gets you the best return based on your goals.

Before entering the investment property market, you should know what you want to achieve and when – i.e. define your goal.

You need to find out how much you can afford to invest, what returns you want to achieve, and a projected timeline of when you’ll need to see those returns. From here, you can evaluate how any potential property might impact your overall wealth and financial future.

How do you determine your financial goals? Think about why you want to invest in property:

These foundational ‘timeline’ questions are crucial to knowing where to look, what to look for, how you structure your finances, and even understanding how much work you’ll need to put in. Deciding your ‘why’ is the first step!

Investing in property is usually for several different financial benefits; capital growth, income from rent, or taxation advantages. As we touched on previously, your financial goals will tie directly into your chosen strategy. Let’s break down your strategy options.

Capital growth happens when your property increases in value over time. This is the primary goal of most property investment, whether the investor is looking to sell in the future, draw on the equity, or simply benefit from the increase in foundational wealth that the property adds to their portfolio. Capital growth is a long-term strategy; Corelogic reported that the average property that sold for a profit in 2022 was owned for 9 years.

Location is absolutely critical, because capital growth is not guaranteed. Many investors find themselves in a situation where the house does not appreciate. If rental income also doesn’t cover the costs, they experience a net loss year on year.

If you’re purchasing a property to earn an ongoing income, you’ll want to choose a property based on your projected rental yields. To calculate rental returns, use the following formula: (weekly rent x 52) / market value of property x 100 = rental yield percentage. For example, if you purchase a property that earns $550 each week, and the property is worth $865,000, this would look like ($550 x 52) = $28,600 / $865,000 x 100 = 3.3%. This rough calculation can be used to evaluate the yield potential between different properties.

Calculate rental returns: (weekly rent x 52) / market value of property x 100 = rental yield percentage

However, this number doesn’t take into account the costs associated with purchasing and owning the property, so a more accurate figure to estimate if you’ll be making a profit from the property (positive gearing) is to add up your property costs and factor them in as an expense. If your net income from the property is less than the property is costing you, that means the property is negatively geared (making a loss). As we mentioned in the capital growth section, you should avoid a property that will continue to make a loss on rental yields indefinitely, unless you will see significant capital growth over that time.

Another reason that investors buy property is for tax benefits. The Australian Government has a number of different tax deductions available for rental properties, such as depreciation, management and maintenance, home insurance, borrowing expenses, interest on investment loans, and more. This is usually a strategy for high-income earners, but the tax offsets of owning property can be used by almost any property investor.

Negative gearing occurs when the expenses of purchasing and maintaining an asset, including the interest on your loan, exceed the income generated by the asset (creating a net ‘loss’). With negative gearing, you’ll have to be able to afford to hold an asset that isn’t ‘earning you income’, but the benefit you get is the ability to offset your ‘losses’ against your taxable income, increasing your tax deductions.

Positive gearing is the opposite – you’re making a profit on your investment, but you’ll also be paying tax on that profit. This is often more affordable for an average or lower income, as the additional cash flow outweighs the tax implications. But for those who are earning a higher income, this could mean you pay more tax (some high-income earners choose a negatively-geared property as a tax offset). However, all investors will want their property to become profitable at some point, rather than being an ongoing drain on cash flow.

If you’ve purchased a property before, you’ll have a good understanding of the process and paperwork. With an investment property, your finances will be slightly different and you may have a few options you didn’t have before.

If you’ve paid off a chunk of your current mortgage, or your existing property has increased in value, you might have equity available to draw on. Equity is the difference between what you still owe and the current value of your property. A lender will usually allow you to borrow around 80% of the value of your property, less your outstanding mortgage.

Calculate usable equity: (80% x property value) – outstanding mortgage = usable equity

Calculate it this way: if you own a property worth $900,000, and your remaining home loan is $300,000, you’ll be able to access equity of $420,000. To calculate your usable equity, follow this formula: (80% x $900,000 = $720,000) – $300,000 = $420,000.

Your equity can go towards a deposit for your investment property. You can also use your equity in a debt-recycling strategy.

When purchasing an investment property, it’s best to save up a deposit that is 20% of the property’s value to avoid Lenders Mortgage Insurance (LMI). This one-off payment protects the lender in the event that you can’t meet your loan repayments, and it is usually required if you have a loan to value ratio (LVR) over 80%. LMI is often higher for an investment property.

If you want to check your LVR, there are many calculators available. To illustrate, I checked an investment home loan of $800,000 against a property worth $900,000 (with a deposit of $100,000). The LVR is 88.8%, and the lender’s mortgage insurance estimate was $17,200 (for a first home with the same LVR, the LMI was $15,600). While LMI can be a beneficial tool to purchase a house even without a full deposit, try and avoid this additional expense.

The most important thing is, of course, what can you afford? I recommend getting a clear idea of your borrowing capacity before you start looking for a property. Lenders will calculate how much they are willing to lend you based on your financial situation and history, particularly your assets and liabilities:

Owning an existing property with equity can significantly improve your borrowing power, but keep in mind that lenders are required to add an interest rate buffer of 3 percentage points to your loan interest rate. This reduces borrowing power by about 5% for most people.

As you’re building your budget, consider your cash flow. If your property changes from earning money to costing you money, even temporarily, will you be able to afford it? Include upfront costs like stamp duty and upkeep costs like maintenance or body corporate when calculating the affordability of your investment. I recommend ensuring you have a cash flow buffer when taking on an investment debt to ensure you can weather the ups and downs.

Investment property loans are also usually more expensive than standard home loans, both in borrowing costs and investment rates. This is because lenders see increased risk in an investment property. You’ll have to spend some time finding the best home loan for you. This includes your interest rate and comparison rate, as well as comparing loan features such as:

Your financial situation and structure is the foundation of a lot of these decisions. Should you choose a fixed or variable loan? Do you suit an interest-only repayment plan for a period of time? I recommend seeing a mortgage broker or financial advisor to discuss your options.

Pre-approval is when a lender has agreed to lend you a certain amount of money, subject to conditions. Pre-approval is usually valid for 3-6 months, so you have some time to look for a property or enter an auction. Generally, you need to remember two primary things with pre-approval:

This is when the fun part begins – shopping! It’s also where a lot of the hard work preparing your strategy can pay off. What you want to achieve by the time you’re looking seriously for a property is:

If you have a clear understanding of these questions, then you’ll know how to evaluate the properties that you are interested in. Avoid speculation, and focus on reviewing the abundant research with a clear head (this blog from Different is helpful).

I can’t emphasise enough how important research is. It will provide you with good grounding in what to look for, and help you be on your guard against property ‘gurus’.

This old saying exists for a reason. The location of an investment property can make or break profitability, and it is often the most deciding factor in the purchase. There are some tried and true standards for property which I go back to:

Finding an investment-grade property outside a capital city requires more rigorous research, as regional areas often have less data and less clear trends. Some basic things to look for include:

| Suburban Properties | Urban Dwellings | Rural Properties |

|

|

|

I’ll cover a bit more information on researching the market in the next section.

The property condition can tie directly into how much impact you have on the value of the property. If you choose a fixer-upper and renovate, you might be able to quickly score an increase in value. However, if you’re not interested in renovating, then rule out old or un-renovated houses.

Small properties usually require less maintenance and will allow you to dip your toes in the waters of being a landlord. A new house or apartment lowers the risk of ending up with lots of maintenance to do. Therefore, if you want to build up your experience as a landlord, consider keeping your first rental property small and new.

Residential properties are best for a first rental property. However, there are a variety of types of property you could choose from.

| Residential Real Estate | Vacant Land |

| The most common type of real estate, residential properties are dwellings such as houses, apartments, or vacation homes. 12-month leases and changes to rent prices annually are fairly standard. You’ve probably had experience renting, so this is a good place to start. | If you want to buy unimproved or cleared land, make sure it is in the right place that will see demand in the future. Vacant land requires little upkeep, but it also provides no income. This is best for people who are able to wait to use the land in the future and don’t need to see immediate returns. |

| Commercial or Retail Real Estate | Industrial Real Estate |

| Suitable for more experienced investors, commercial real estate comes with higher costs and maintenance. Secure tenants provide a stable income due to multi-year leases, but financial risk is greater if the property becomes vacant. Long fixed-price lease periods mean you can miss out on improving rental yield | Industrial warehouses, manufacturing facilities, long-term storage units, and carwashes all fall under the industrial real estate title. It can be harder to predict the rise and fall of industrial property value due to external factors, such as large retailer activity. |

Make a list of all the factors that are important to you in selecting the property. Maybe your real estate agent or buyer’s agent can identify quality properties that fit your initial criteria. Then go through the list and evaluate based on your needs:

We’ve discussed location and property types, and now you’ve shortlisted some investment property options. Now it’s time to evaluate each property itself as well as the area or suburb where it is located. Due diligence is the cornerstone of a successful investment, ensuring that you minimise risks and maximise returns.

What’s happening in the suburb or the neighbourhood of the property you’re considering? Start with the more obvious things such as crime rates, good schools, and zoning. Check for infrastructure plans or development in the area that might impact capital growth.

Check the demographics of who is currently living in the neighbourhood. For example, if it’s close to a university, it might be more suited to students than as a rental for families. The demographics of the neighbourhood can tie into your rental yields and vacancy rates.

It’s valuable to research the employment trends and median disposable income for the suburb using CoreLogic and ABS databases. Areas with high employment with higher income often see better capital growth and higher rental yields.

Generally, property travels in a cycle, both on a local and national level. Research purchase price trends, auction clearance rates, and demand to supply ratio (DSR) or days on market (DOM) to see if the suburb is experiencing demand. Buying as the suburb is growing is ideal, but if you are planning to sell the property within a year or two, you don’t want to buy at the peak time. Look out for over-inflated prices; research what similar properties are selling for in the same area and if the median sale price for the area is increasing or decreasing.

Review the condition of the property thoroughly with the help of a professional property inspector and make a note of any maintenance needs or improvements required. Questions to consider include:

If the property already has tenants, review existing lease agreements, security deposits, and rental history. Check for any ongoing disputes or issues with tenants. Once you’ve got a thorough understanding of the properties’ good and bad points, you might have an opportunity to negotiate repairs or purchase prices.

An absolutely vital step is making sure the cash flow of the property will suit your strategy or financial situation. A property that generates positive cash flow is ideal for most real estate investors. If the cash flow won’t cover all your expenses, you’ll need to plan for covering costs and for the future of the property. You should also think about an exit strategy, particularly if your return on investment doesn’t improve.

Calculate your cash flow by subtracting your total expenses from the total rental income. If a property is already tenanted, you could also request the rental history of the property to learn about income trends and vacancy rates.

When calculating your expenses, don’t forget to include things like utilities, property management, landlord insurance, strata or body corporate fees, property taxes, legal costs and advertising costs. These can be overlooked but will dent your profits.

Once you know how much the property will make over the year, take that number and compare it to your budget. With negative cash flow but in a growing area, the property could still pay off for you in the long term. But can you afford to cover the cash flow gap now?

You’ve secured your loan, you’ve gone through the settlement process, and now you’re the proud owner of an investment property. Like Sarah, my client at the beginning of this article, you’ve put the SOLD sticker on the For Sale sign, and you’re about to be a landlord!

Many landlords, particularly those with just one rental property, will manage the property themselves. However, if you are time-poor, or the property isn’t close to where you live, an experienced property manager can make your life a lot easier. Local Agent Finder advises that you’ll pay around 7-10% of your rental income for property management fees.

A property manager can take on many of the responsibilities, such as:

It’s important that you understand the legal and ethical responsibilities that you have as a landlord, even if you are engaging a property manager. You can find more information on the rights of landlords and managing tenancies at the RTA website.

It’s helpful to get professional advice before investing in a large-scale asset. Speaking to a financial planner can help you avoid expensive mistakes like buying in the wrong location or not getting your cash-flow right (and having to sell at a loss). Just as important, you can get help with coordinating your property strategy with your tax, your family goals, your savings and your retirement plan.

Your mortgage broker can help you accurately gauge your borrowing capacity before applying, advise on preparing your financial records to get the best chance for approval, as well as researching loan options and completing your application. They can also negotiate your interest rate and your borrowing capacity on your behalf. Start strong by speaking to a few mortgage brokers early in the process.

A buyer’s agent will do the heavy lifting of research and local sourcing to find a property that fits your needs and budget. With insider connections, buyer’s agents will use your financial and strategy requirements to identify suitable properties both on and off the market.

A real estate agent can be your main source of property information. They can provide you with a list of suitable assets, arrange inspections for you, prepare any contracts, and liaise with the seller on your behalf.

You need to be able to trust your real estate agent. Make sure your agent is working for you, not just for the seller, and beware of property groups and spruikers that make huge commissions from selling low-quality properties to you. Your agent should focus on your priorities, know the market well, and be honest and direct.

A property inspector visually inspects a property for damage and makes sure it complies with legal obligations. The property inspector will give you a report on the property, confirming everything is as it should be or listing all the changes that will need to be made. A pre-purchase building and pest inspection can make or break a purchase.

Property managers take care of day-to-day tasks to maintain the property and manage tenants. When negotiating a contract with a property manager, you can pre-approve a certain amount of maintenance costs per set period of time. That means you’ll have to approve fewer requests and can manage your budget in advance.

Navigate the process with ease by speaking to one of our financial advisors today. With specialists in property as an investment strategy, our team will be able to help you prepare and find the right property to grow your wealth.

Guy is Co-CEO at My Wealth Solutions. He takes a genuine interest in his team and works one-on-one with each financial advisor.

B. Biomedical Science, Dip. FP, Adv. Dip. FP, SMSF

View my profile